Senate Banking Boycott Threatens Biden's Scandal-Ridden Fed Board Nominees

Senate Banking Boycott Threatens Biden's Scandal-Ridden Fed Board Nominees

Vice Chair nominee Brainard is conflicted as to massive financial firm Blackstone; Powell, Brainard & Raskin should all be disqualified from public office

Presidents’ Day is a great time to remember that most of America’s founders never wanted a central bank like the Federal Reserve. Alexander Hamilton, who is now more famous than most Presidents but never held the office, created the first national bank. It failed within 20 years of being formed in 1791.1 The U.S. Constitution certainly does not provide for the Fed. Many legal scholars agree the Fed is, in fact, unconstitutional. It was only created by Congress in 1913 after a group of big bankers secretly devised the plan during a creepy, private gathering at Jekyll Island.

Congress is supposed to oversee the Fed — a massive and growing swamp creature with both a public agency “Board of Governors” (that supposedly serves the American public) and twelve Fed “Regional Banks” (that answer to private bank stockholders, i.e. Wall Street megabanks like JP Morgan in the case of the New York FRB). The Fed system has more than 20,000 employees, including trading desks in New York and Chicago, and supposedly regulates our biggest banks. The Fed’s balance sheet is nearly half the U.S. GDP at almost $9 trillion now (bought with money that Chair Powell said on 60 Minutes is “printed digitally” to “flood the system”). Suffice to say, the Fed has metastasized into something far more than an agency that simply promotes “maximum employment” (which the Fed refuses to define) and “stable prices” (which supposedly means roughly 2% inflation — epic fail!).

Congressional Oversight of the Fed Is A Complete Joke

The Fed’s size and (over)reach make Congressional supervision vital. But thirteen years after the Global Financial Crisis that the Fed helped create, the Senate Banking Committee and the House Financial Services Committee are a joke. Where are the inquiries, investigations or subpoenas to the Fed after two years of the most radical and reckless monetary policy ever or the worst scandal in Fed history? Their hearings are all little more than political grandstanding.

What’s the end result? A Fed that does whatever Wall Street wants, even if it destroys the American middle class or destabilizes the entire financial system. A Fed that the American public now sees as actively manipulating the “free markets” with secret interventions and bailouts. A Fed where the rules and ethics are so loose that senior officials with access to material non-public information — including Fed Chair Powell himself — caused a sprawling insider trading scandal, increasingly referred to as #Fedgate.

Quite simply, the Fed is out of control. There is no transparency. There is no accountability. Fed Chair Powell and his cronies think they are above the law and answer to no one but Wall Street CEOs like BlackRock’s Larry Fink.

Fed Chair Powell acts with such impunity that, since October 2021, he has blown off three different letters from a Senate Banking member demanding details about the illicit Fed official securities trading. The Fed has stonewalled multiple journalist FOIA requests seeking details as well. At the hearing on his renomination in January, Powell admitted to Senator Jon Ossoff that the Fed did not even bother to send a draft of updated trading rules to Senate Banking. (Most major news outlets hope you forget the “trading blackout that already exists in the days around meetings of the policy-setting Federal Open Market Committee” that Powell himself violated).

Instead, the Fed chose the Friday before President’s Day to sneak out the trading rules — which are wholly inadequate and riddled with loopholes. The Fed sent them to select media outlets to run puff pieces talking up how “strict” they are, while ignoring a FOIA request from Walter Shaub, former Director of the Office of Government Ethics (OGE). Mr. Shaub unveiled at least 14 fundamental problems with the Fed’s new trading rules based on his initial review. The rules provide for blanket exemptions with no definite standards, making them likely worthless in practice. We find it very interesting that the exemptions appear most generous for family trusts — the very tool Powell uses to manage the bulk of his $100 million wealth in personal stock holdings — even though such trusts are not exempted from OGE requirements.

This all a gross perversion of the “independence principle” for Fed monetary policy. Ethics rules and violations are threshold governance issues. Chair Powell certainly should not be overseeing any of this process after he presided over and is implicated personally in scandal. Congress needs to wake up and take control immediately.

While Congressional oversight of Fed ethics is atrocious, oversight on policy might be worse. Even Senate Banking doesn’t seem to know or understand what the Fed is doing. Why did it take an inflation crisis for Senate Banking to start asking the Fed about more than doubling its balance sheet to $9 trillion, long after the stock market blew past all-time highs? At Powell’s hearing, Senator Thom Tillis quoted Atlanta Fed President Bostic as saying the Fed should “aggressively draw down the balance sheet by $100 billion per month.” Then Sen. Tillis suggested that the Fed had started to reduce its balance sheet and “went up from $15 billion to $30 billion…”

Tillis was flat wrong. The Fed only started to “taper” its extraordinary “Quantitative Easing” (QE) purchase program of $120 Billion plus per month in Treasurys and mortgage-backed securities. The Fed is not shrinking its balance sheet at all yet. Since announcing its taper, the Fed added $332 Billion in new purchases — the equivalent of a quarter point interest rate reduction — as reported by Wall Street on Parade. It’s absolutely no wonder why inflation continues to skyrocket.

Powell made virtually no attempt to address the Senator’s error or correct the record under oath. Why? Because if the public really understood what was going on here, there’d be mass outrage. Instead, the Fed continues to say one thing, and do another. You can watch the full Tillis-Powell exchange here.

Powell Is Unfit for Public Office — So Is Brainard

As we’ve detailed in our prior articles, Powell irreparably violated the public’s trust with his trading and ethics violations and should be fired immediately. Because of his intentional obstruction, we still don’t even know the extent of his FOMC blackout trading. And as former Fed insider and analyst Danielle DiMartino Booth said, Powell’s flawed explanation for the dozen trading violations we uncovered two weeks ago is simply not credible:

Powell should have confessed and resigned by now, but apparently the buck doesn’t stop with him. Indeed, a culture of corruption at the Fed is pervasive. Take Fed Board Governor Lael Brainard, who is up for Vice Chair. Some have suggested Brainard is above board because, unlike Powell who dumped more than $1 million in securities just before a market pullback, she made no securities trades in 2020 (that we know of) during pandemic market turmoil. This is ridiculous.

Even cursory looks at Brainard’s prior disclosures reveal dozens of securities trades in between key policy decisions — many just a day or two before or after the FOMC trading blackout. Brainard made a staggering EIGHTY-FIVE (85) securities trades in 2016 and EIGHTY-FOUR (84) trades in 2017.2 But wait, there’s more.

In 2018, as the Fed made its biggest decisions on interest rates since the Great Financial Crisis, Governor Brainard made a record-shattering ONE HUNDRED THIRTY-THREE (133) securities trades.3 No Fed Board Governor has any business trading that actively, especially in the midst of major, market-moving policy decisions. But wait there’s more, and it’s worse.

Brainard’s husband is Kurt Campbell, who is also President Biden’s “Asia Czar” or National Security Council Coordinator for the Indo-Pacific. Brainard and Campbell have been married for more than 20 years and are quite the DC power couple. They used to run a consulting business out of their house. Before Brainard was confirmed for a top Treasury job back in 2009 in the Obama administration, she actually got some heat from Congress about late property taxes and the accuracy of the deduction they took for their home consulting office.

Kurt Campbell also landed a government gig in 2009 at the State Department as Assistant Secretary for East Asian and Pacific Affairs. In 2013, up to a month before leaving public office, Campbell founded a new company called “The Asia Group” to make investments and advise corporate clients. While beyond the scope of our article, the Project on Government Oversight (POGO) has an incredible exposé on Mr. Campbell’s “Troubling Business Connections” that is well worth the read here.

In short, among other things, Campbell appears to have used his role at the State Department to soften sanctions on Myanmar before The Asia Group bid to renovate the country’s airport, peddled his influence with other clients having business interests in Asia, and then failed to divest his holdings in The Asia Group before being appointed as Biden’s Asia Czar in January 2020. As the POGO article states:

“Campbell’s financial disclosure form…which was amended twice after we requested it, paints a troublingly incomplete picture…The Asia Group bears all the hallmarks of a ‘shadow lobbying’ outfit, one that provides behind the scenes assistance to its clients to help secure government contracts and to otherwise bridge the gap between government and businesses.”

Jeff Hauser, head of the Revolving Door Project, is quoted in a Washington Free Beacon article as saying the conflicts from the failure to divest from The Asia Group are “atrocious … You have a powerful government figure with a direct way to profit that is pretty obvious. He absolutely should have no ties to any consulting company.” Campbell reportedly received more than $1.6 million from The Asia Group in 2020!

Brainard Is Inexcusably Conflicted As To Massive Firm Blackstone Group

Why does all this matter? Because all of Campbell’s conflicts are imputed to Brainard by law. And how could that conflict influence a Fed Vice Chair you might ask? In a lot of ways, particularly with respect to how policy decisions impact her husband’s corporate clients in general. But here’s another very clear, specific problem — Brainard is now conflicted as to Wall Street behemoth Blackstone Group!

In 2020, Campbell decided to accept two $25,000 payments from Blackstone Group for private speeches. Campbell’s initial 2021 OGE filing failed to report them at all. That omission is seriously disturbing and unexplained. And in many ways, this conflict has far greater implications for Brainard than Campbell.

Blackstone Group is a massive private equity firm that may reach over $1 TRILLION in assets this year. Blackstone is America’s largest landlord and has been busy buying up every affordable single-family home it can find. More than ever, Blackstone is engaging in what’s called “shadow banking” — making large loans outside the parameters of a traditional bank. Blackstone is busy securitizing rental income streams from its real estate acquisitions in ways painfully reminiscent of the massive housing crash during the GFC.

Because Blackstone engages in shadow banking, it is not yet subject to the same rules and regulations as investment banks. Indeed, pay and bonuses at private equity firms like Blackstone, BlackRock and Caryle Group (where Powell worked before the Fed) is astronomical. Blackstone’s founder Stephen Schwarzman took home an insane $615 million in compensation for 2020. Even investment banks like Goldman Sachs are having trouble competing to retain talent.

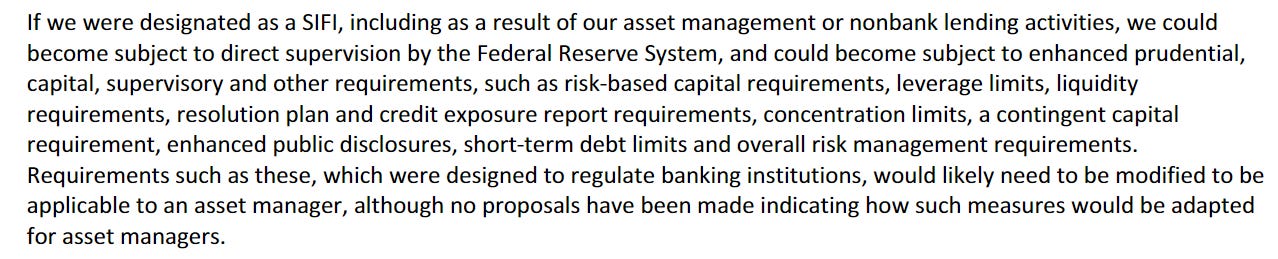

The possibility of the Federal Reserve finally stepping in and regulating Blackstone is so important that it is one of the firm’s key risk disclosures in its annual 10-K. The “Financial Stability Oversight Committee” — formed after the GFC and on which the Fed Chair sits — has the ability to designate nonbank financial companies as “Systemically Important Financial Institutions” or SIFIs.

It is a shocking truth that private equity firms like BlackRock and Blackstone, which engage in astronomical amounts of shadow lending and have more assets under management that most of the largest U.S. banks, are not yet designated as Systemically Important Financial Institutions. If and when they are, they will be subject to “direct supervision by the Federal Reserve system” and “could become subject to enhanced prudential, capital, supervisory and other requirements…”

In June 2020, Brainard herself joined Treasury Secretary Yellen on a panel and stated that the U.S. government “dropped the ball” on regulating private equity shadow banking, which was a primary cause of the GFC. Just three months later, Blackstone paid Brainard’s husband $50,000 for his two private speeches.4

Given the timing, we find it very disturbing that these payments were not disclosed properly in the first place. We can only imagine the conversation between Brainard and her husband: “Hey honey, Blackstone said they’d pay me fifty grand to give two dinky talks. Maybe you should cool off on the whole ‘shadow banking’ critic thing.”

And it leaves us to wonder what else we don’t know about Mr. Campbell and Ms. Brainard. Like, what is Sea Futures LLC? For all we know, it’s a company that trades US stock market futures on a boat in international waters.

What we do know is clearly enough to disqualify Ms. Brainard. Unless you think it’s somehow appropriate for our Fed Vice Chair to be conflicted under 18 U.S.C. § 208 from making decisions with respect one of the biggest financial firms in the country and one of the most important regulatory issues of our time — unregulated shadow banking by private equity behemoths. We certainly don’t that’s appropriate.

GOP Derails Biden’s “Fed Five” Over Raskin Influence Peddling

Finally, the big news last week was that Republican Senators on the Senate Banking Committee boycotted a meeting needed to move Biden’s Fed Governor nominations to the floor for a full Senate vote. Ironically, zero Senators — Democrats or Republicans — have raised any issue with the major conflicts or violations we have covered for Powell and Brainard. The GOP has, however, zeroed in on Sarah Bloom Raskin, who has been nominated for the key role of Vice Chair for Supervision after having served as a Fed Board Governor from 2010-2014.

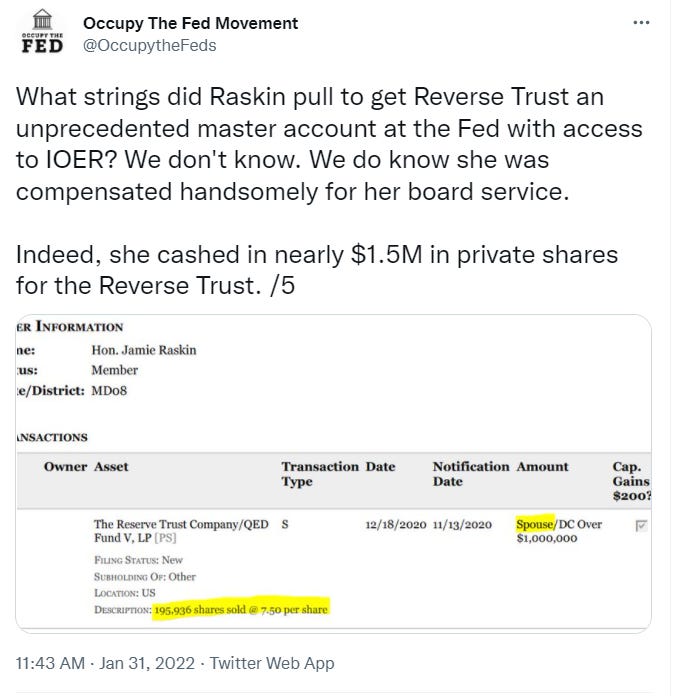

To our knowledge, the Occupy The Fed Movement was first to report on Raskin’s apparent revolving door, influence peddling in this short Twitter thread. At Raskin’s confirmation hearing, Senator Cynthia Lummis proceeded with a gritty line of questioning about Raskin’s role on the “Reserve Trust” company board — the first and only fintech to obtain a Fed master account (and the benefits associated therewith). Raskin cashed in nearly $1.5 million in private shares for her service on the company board, as has been detailed by various major news outlets at this point.

We think Raskin might have done a fine job at Vice Chair for Supervision. But why must we continue to accept unethical behavior from our Fed officials? Why can’t the President nominate others who haven’t apparently used their positions at the Fed to enrich themselves? There are still good people left in this country who are willing to sacrifice personally in service of the American people.

We hope our Senators stop gaslighting the American public into a bogus all-or-nothing choice between the #FedFiveNow or nothing. It’s wrong and shameful. It’s especially asinine to suggest that a delay in confirming better qualified Fed officials would have anything to do with skyrocketing inflation. Powell is currently Fed Chair Pro-Tempore. Brainard is still a Governor. The FOMC could stop buying tens of billions in debt securities and raise rates in 15 minutes if it wanted.

But inflation is never an emergency to rich Fed officials and their ultra-rich cronies — no matter how much it decimates the American middle and working class. But the problem of the Federal Reserve has become a national emergency that threatens the very survival of our democracy. Our founding fathers would be appalled that our elected politicians don’t seem to give a damn. It’s time to wake up, America.

The musical Hamilton is delightfuly, but conveniently leaves out the demise of the first national bank and that the Federal Reserve became the “greatest driver of wealth inequality in history.” https://www.federalreservehistory.org/essays/first-bank-of-the-us

The greatest irony of it all is that they give the illusion it is a public office, yet there is nothing Federal about them nor do they have any Reserves! Owned by the big Banks themselves. Their house of cards is coming down, slowly at first, and then it will happen very quickly all at once!

☕✝️