The Fed's No-Limit Bank Bailout Repo Scheme - $20 Trillion and Counting

The Fed's No-Limit Bank Bailout Repo Scheme - $20 Trillion and Counting

How the Fed wants to bail out the world's banksters again with standing repo facilities

This week, after President Biden’s State of the Union, Fed Chair Pro-Tempore (for now) Jerome Powell will appear in hearings before Congress on Wednesday and Thursday to provide an annual update on Federal Reserve monetary policy. The state of Fed policy could be summarized in one word: INSANE. Instead, it will go something like this. Senators and House Reps will ask softball questions and grandstand about how fiscally irresponsible their colleagues are across the aisle.

And Powell will respond something like this: “I’m a hero for saving the economy in the pandemic [even though all we did is ensure Wall Street and the ultra rich profited from crisis for 2 years while Main Street got peanuts from Congress]. The pandemic disrupted supply chains and caused rampant inflation [even though the has U.S. worse inflation than almost every other country in the G20 other than Argentina and Turkey, which are dealing with the same or worse supply constraints]. And we’re very serious about taking action on inflation soon [even though all we’ve done is talk about it while still pumping tens of billions in QE and keeping rates at zero for megabanks].”

Nobody will ever ask, but here are a few policy questions we have for Jay:

If the war in Ukraine is certain to make inflation worse and backstopping the stock market is not part of the Fed’s mandate, why doesn’t the Fed speed up its long overdue shift from maximum accommodation to quantitative tightening?

Do you see why people might think Fed policy is designed to enrich Fed officials and their cronies on Wall Street, especially after the Fed insider trading scandal and your own trading violations?

Why is the Fed STILL buying tens of billions in mortgage-backed securities on top of the $2.7 trillion they bought despite at least 15-20% housing inflation? And why does the Fed hold a quarter of all U.S. mortgages on its balance sheet?

What’s to stop the Fed from recklessly expanding its balance sheet again, after doubling it to $9 trillion in 2 years, and after refusing to shrink it meaningfully in the decade plus after the Global Financial Crisis?

Why is the Fed STILL allowing zero reserve banking 2 years after the pandemic “emergency” prompted a change in policy from fractional reserve requirements?

How was the nearly $20 trillion in cumulative repo loans the Fed doled out in late 2019 not an illegal megabank bailout?

The Fed’s $20 Trillion Repo Megabank Bailouts

There’s a story the media refuses to report on that’s bigger and involves way more money than Jay Powell brazenly violating multiple FOMC financial trading blackouts without apology. And that’s the Fed’s massive, secretive $20 trillion repo bailout program in late 2019 — before the COVID pandemic even started. The public deserves to know the full story about both of these outrageous events.

Yet zero financial news outlets will even mention the scandals, apart from one. Wall Street on Parade (WSOP) has provided incredible, ground-breaking coverage of the Fed’s megabank bailouts with far better analysis and insights than we could hope to muster. If we didn’t live in a bizarro reality where Wall Street and its monstrous, multi-national firms have taken over the world and its media, WSOP would have a shelf of Pulitzers. If you haven’t read their articles on it yet, prepare to be outraged. They have tons more, but these three should help get you started:

“A Nomura Document May Shed Light on the Repo Blowup and Fed Bailout of the Gang of Six in 2019”

In sum, as WSOP reported: “there was no ‘broad base’ of the U.S. financial system being bailed out by the Fed in the last quarter of 2019: 62 percent of a cumulative $19.87 trillion in rolled-over repo loans went to just six trading houses: Nomura Securities International ($3.7 trillion); J.P. Morgan Securities ($2.59 trillion); Goldman Sachs ($1.67 trillion); Barclays Capital ($1.48 trillion); Citigroup Global Markets ($1.43 trillion); and Deutsche Bank Securities ($1.39 trillion).”

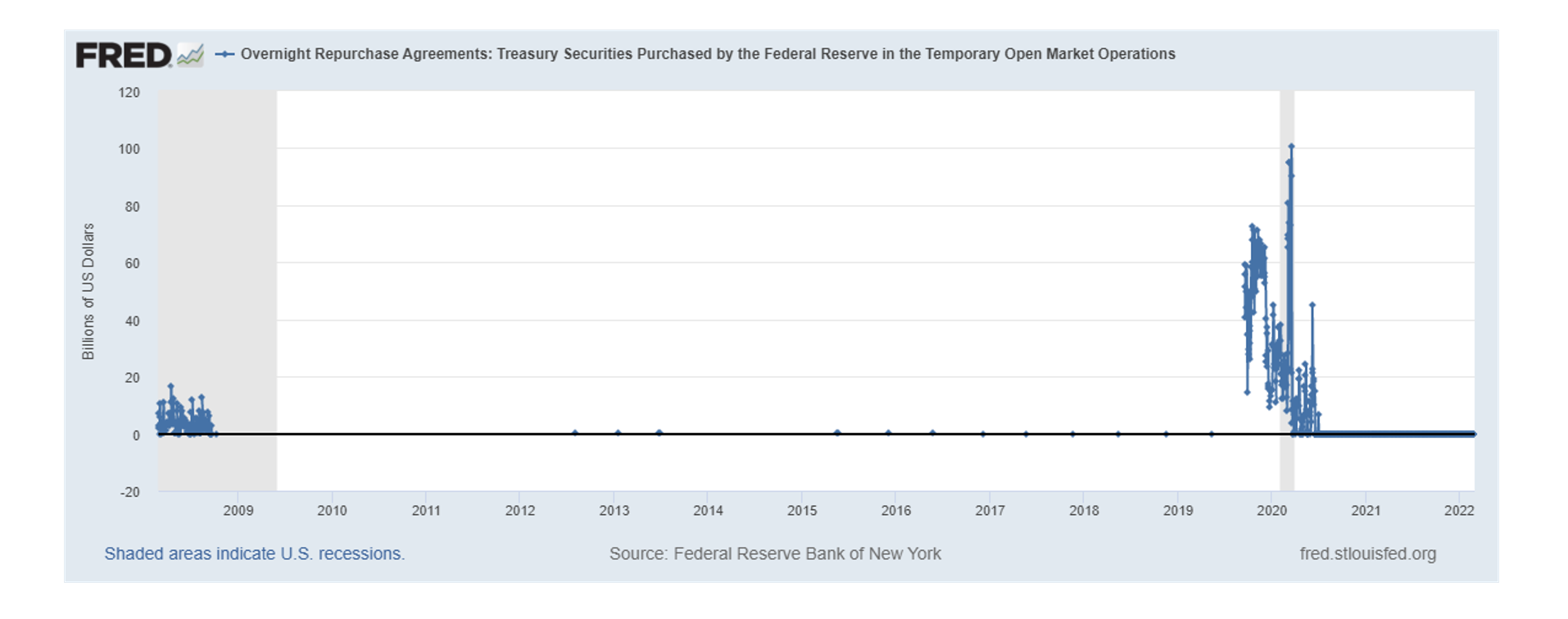

It all started when, in September 2019, JP Morgan broke the repo market, spiking the secured overnight financing rate in the U.S. to 10% like in say Brazil or Argentina, after the “too-big-to-fail giant made a pivot out of cash into securities.” The WSOP coverage suggests that this event might be connected to something going terribly awry in the shadowy and highly risky derivatives market. Instead of addressing five-time felon JP Morgan’s blow up transparently, the Fed decided to flood the market with cheap, non-market rate repo loans in an attempt to cover it up. The Fed claimed these were “purely technical measures” — just an innocuous plumbing issue. Right.

The loans went to the usual suspects on Wall Street — U.S. megabanks JP Morgan, Goldman Sachs, and Citi — which, after getting bailed out in the Great Financial Crisis, continue to make massive, risky bets on derivatives. It’s totally unacceptable that the Fed orchestrated a stealth bailout of this magnitude. Economist Michael Hudson has opined that the Fed actually “broke the law” with its repo bailout operation. Indeed, the Dodd-Frank Act was supposed to limit the Fed’s ability to engage in emergency lending programs unless it was for a “broad base” of solvent financial institutions during a period of financial crisis.

But no matter what ridiculous spin the Fed and their apologists put on it, this was no ordinary “technical” issue. The Fed itself admits: “Other than occasional test operations, the FRBNY had not conducted a repo since December 2008.” Just one look at the charts, and it’s obvious the Fed was engaged in a massive emergency lending program for a select few Wall Street megabanks — far exceeding the Great Financial Crisis in 2008 and before the COVID pandemic hit in 2020.

What may be even more disturbing is the U.S. Fed’s decision to extend trillions in risky loans to the trading arms of big foreign banks — particularly Nomura in Japan and Deutsche Bank in Germany. The Dodd-Frank Act was very clear that the Fed was only to provide emergency loans “for the purpose of providing liquidity to the financial system, and not to aid a failing financial company.” Nomura was roughly 90% exposed to derivative risk when the Fed extended $3.7 Trillion in repo loans to its trading arm. Deutsche Bank was on the brink of total collapse when the Fed extended it $1.39 Trillion in repo loans.

Just like its repo bailout, the Fed’s risk tolerance for taxpayer money is off the charts. The American public deserves to know. Congress should be investigating the matter. We’ve been in contact with reporters at various major financial news outlets, and the responses as to why they won’t cover this story are deeply unsatisfying:

WSOP has openly wondered if major outlets have their journalists under gag orders. Given the fact that, among others, BlackRock owns large stakes in a dozen news companies and Blackstone wholly owns Reuters, we agree that’s entirely possible.

The Fed’s New Standing Repo Bailout Facilities

Now the Fed wants to normalize megabank bailouts by creating standing repo facilities for private banks and even foreign central banks to tap at any time. Last July, the Fed announced the creation of two new lending facilities - a Standing Repo Facility (SRF) with a supposed $500 Billion limit and a similar standing facility for Foreign and International Monetary Authorities (FIMA) with a “mere” $60 Billion per entity limit. This is an unprecedented move that, as usual with the Fed’s dealings, has gotten far too little attention or pushback.

What’s to stop the Fed from blowing through artificial limits to their intervention in our supposedly “free markets” like always? Why do supposedly “well-capitalized” U.S. banks need a permanent repo backstop? What exactly is the U.S. Federal Reserve doing lining up bail outs for the trading arms of foreign banks and even foreign central banks?! Back in late 2020, former Vice Chair for Supervision Randy Quarles had cast significant doubt on the SRF. Now the Fed has done an about-face, just as it jawbones about normalizing policy and shrinking its $9 trillion balance sheet.

So far, zero repo loans have been made pursuant to the new facilities. According to the Bank Policy Institute (BPI), the industry is supposedly “skeptical that the SRF would be successful. While all primary dealers have access to SRF, to date, only three banking institutions, in each case an affiliate of a large broker-dealer, have signed up to use the facility. Banks and primary dealers are concerned that borrowing from the Federal Reserve will be held against them by their examiners and by the public.” Indeed, BPI has suggested that the “shame” of tapping the discount window or SRF might be a major limit on the Fed’s crisis toolkit going forward. Good — the Fed’s actions to date are truly shameful.

But the fact remains that usual bailout suspects Goldman Sachs and Citi have already lined up for the SRF. Just a week ago, the Fed added Bank of America to the list. And BPI has suggested that the Fed might reduce “the facility interest rate so that it [would be] used regularly, not just in emergencies.” We can all see where this is heading — more bailouts for Wall Street (which just lavished its execs with the biggest bonuses in history) at the expense of the American middle and working class.

When are we going to say enough is enough? Every incumbent Senator is complicit with the Fed’s corrupt and destructive monetary policy if they vote to reinstall Chair Powell and the status quo at the Fed. And we all must tell them we know what they’re doing and hold them accountable at the ballot box in November.

#OccupyTheFed

Great article. Thanks for the work you're are doing.

Great article. only the elites in high finance care and understand about this stuff. We need to make it more understandable and appreciate by everyday Americans. Have you heard of Bankless? I think this may be a beneficial match. They have a strong vibrant crypto community rooted in distrust of the current financial system and self sovereignty. https://newsletter.banklesshq.com/

Let me know if you need connections.